Market Recap

Two years ago, the world was forced to grapple with Covid-19. No one could imagine the life altering impact of the pandemic on every aspect of our lives. Trite as it sounds, things will never be the same. In the last two weeks, as Russia has attacked the Ukraine, we are living through a similar moment that will have profound impact on the world and the financial markets for years to come.

We are appalled by Russia’s attack and our hearts are broken for the innocent victims of the conflict. There will be ample time to consider how the world got to this place and how a repeat can be avoided. At this time, our role as advisors is to consider how this event will impact economics and financial markets as we move ahead. As with Covid, there will be many surprises along the way, but if we set aside wishful thinking about “getting back to normal” we believe that the long- term impacts of this attack will change the economy and markets for a very long time.

The most immediate impact is on inflation and the supply chain crisis that has plagued the world since we met Covid. Russia is a vitally important exporter of oil and natural gas. In a world that was already struggling with rising costs for energy and the challenge of a transition to “green” fuels, sharp disruption in the market is met with sharp increases in prices. As we write, oil prices are approaching $130 per barrel and natural gas, particularly in Europe with its greater reliance on the Russians, has positively exploded in price. These spikes are very destabilizing for economies and are very difficult for policy makers to address.

Economically, Jim Bianco has pointed out that in the last fifty years, every recession was not preceded by an energy price spike, but every energy price spike of this magnitude has led to a recession. The consensus, of course, doesn’t see a recession but it never does. With this variable, we find ourselves on the eve of the Fed beginning to raise interest rates to combat inflation. Nearly always late to the fight, the Fed again seems to be ready to do something that should have started this time last year. Now, they are in the uncomfortable position of tightening at a time when they would likely prefer to stand down. Given the magnitude of the inflation problem that they allowed to spread prior to the Russian attack, however, they are left with little choice.

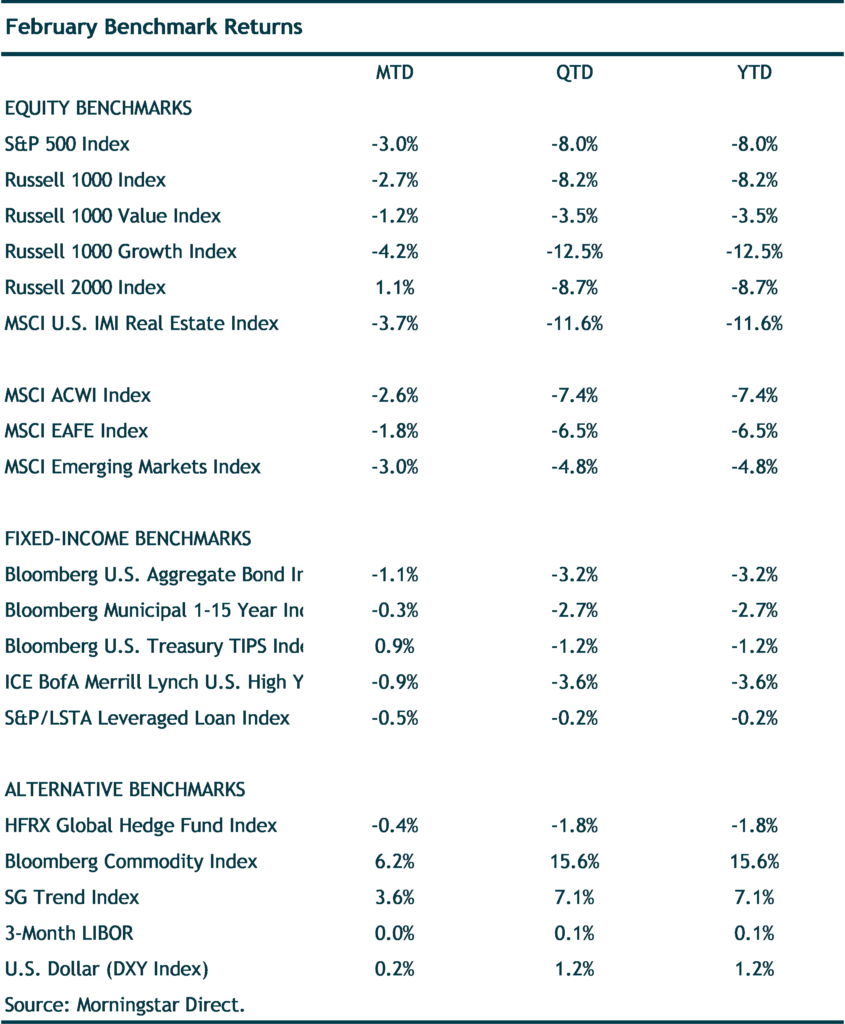

Nervous investors have flocked back to Treasury bonds in the past few weeks and the yield curve (the difference between short and long term rates) is nearing an inversion. Inverted yield curves have a perfect record of predicting recessions. Knowing this, equity market weakness is much easier to understand. Stagflation, the condition of weak growth coupled with uncomfortable inflation reading, is the worst of all worlds for policy makers and investors.

This outbreak of war seems to further seal the fate of globalization and the belief that through economic interaction, peace and security could be maintained. The tide has been going out on these ideas for some time, and the pandemic and impaired supply lines only heightened those issues. Now, however, we can see that playing nice and worrying about markets and GDP growth doesn’t matter to a villain like Vladimir Putin. The capacity to produce on shore is more than economic advantage. It is a security imperative and costs be damned! And that is also inflationary.

Russia was likely surprised by the scope and extent of the unified Western response. The stated unwillingness to engage militarily has clearly given Putin the “space” to proceed with this attack, but the sanctions that have been imposed will be crippling to Russian economy as we move ahead. The righteousness of the sanctions isn’t in question, but there are several aspects of this exercise that give us pause. Broadly, these developments can be described as the weaponization of finance.

History has shown that financially crippling a country can lead to desperation and destabilization. That isn’t a reason to avoid painful penalties, but law of unintended consequences has not been repealed. Will a desperate Russia become aggressive with cyber attacks or other forms of hostile action with the West? We must all be prepared for that possibility.

More immediately, the moves to freeze Russian financial assets will have a profound impact moving forward. Cutting Russian banks out of the SWIFT network will be crippling for many institutions, but that will have knock on impact on counter parties in Europe in particular. The larger issue, however, is freezing Russian central bank assets. Seizure of these assets is a clear message around the world that the Western financial system will take your property if you don’t play by the rules. How can this development not cause every country to re-assess the wisdom of holding assets in foreign countries and with foreign central banks? China, with ownership of more than $1 trillion on Treasury securities, must be looking at these developments with great alarm. We would suspect that Chinese ownership of US assets has peaked and that may have significant long-term implications for the dollar’s status as the reserve currency across the globe.

On a more granular level, there has been much cheering about “seizing” the assets of the “Russian oligarchs.” Seldom is heard any objection to this act of retribution but we are troubled by the news. We believe fervently in the rule of law. We believe equally that guilt by association is not a punishable crime. On that basis, when we see Russian citizens, regardless of their net worth, having assets seized by Western governments (They own a yacht! Take it!), we wonder what the legal rationale is for the seizure. If property was used in the commission of a crime, or acquired with ill- gotten gains, then by all means use a judicial process to seize the asset. We worry, however, that absent the protection of the law, it is hard to know where the indignant, righteous mobs may turn next. It is also hard to know whether or not our adversaries may turn the table on us. Might the Chinese government decide at some point that US owned property in China would be useful in the drive for common prosperity? We don’t know if this will come to pass, but even the possibility introduces a level of risk that hasn’t been priced into the markets.

We continue to monitor developments closely. These are the periods that test investors but prove the value of diversification and a focus on value. It is difficult not to read current developments as leading us toward being more conservative than we have already been. As always, we welcome your comments and questions and are grateful for your trust and confidence in the face of turbulence and uncertainty.

How does this impact portfolio positioning?

If easy money is going away, or at least going on vacation, we think investors will be rewarded by favoring high quality investments, remaining diversified and being “close” to their cash flows. When we say be close to your cash flows, we would contrast a high- quality consumer staples company sporting a well- covered and growing dividend with a speculative electric vehicle company (think Rivian) that has yet to build or deliver on the promise of their earth saving autos and trucks. When capital is cheap, a flyer on the latter can make sense. When capital is more expensive, we hope and believe that fundamentals will be the key driver of assets returns. That belief will continue to inform our recommendations to you.

A Note on Taxes

It is hard to believe that it is time to begin discussing taxes but the 2021 tax return filing season is upon us. The old adage that the early bird gets the worm may be valuable advice, but in tax filing, the early bird often gets to amend their return. Schwab and other custodians are in the process of sending out tax reporting data. While they work hard for accuracy, they are often required to issue the dreaded “corrected” 1099 as they receive updated information from fund managements.

We look forward to assisting you in gathering the data to make the tax filing process as smooth as it can be. Please let us know if you have questions or concerns as your data arrives and remember that many documents are now delivered via email as well.

Up Next...