A chaotic and uncertain world has become dramatically more uncertain in the last two months. While there are many storylines capturing investor attention, none are more meaningful than the conflict in the Middle East.

The United States and Israel attacked Iran with a dramatic “shock and awe” bombing campaign at the end of February. The conflict continued throughout March with varying intensity, at times appearing to ebb before quickly re-escalating. The Iranian leadership was decapitated on the first day without a clear line of succession, creating additional uncertainty about who is making decisions and what strategic objectives now guide Iran’s response. Iran retaliated with missile and drone attacks throughout the Middle East, targeting many countries that were ostensibly neutral in the conflict. While the US and Israel have made real progress toward the goals of eliminating the ability of Iran to finance terrorism and project force, the ongoing capacity of Iran to threaten neighbors and disrupt shipping through the Strait of Hormuz still exists.

A tenuous ceasefire began in April. Where it stands now seems to be anyone’s guess. While missiles and bombs aren’t flying with the same frequency, both sides trade claims that leave observers dizzy. Iran seized control of the Strait of Hormuz and threatens attacks on ships that don’t pay tolls. The United States, in response, has imposed a blockade of its own. According to their social media accounts, both sides seem to believe they hold the upper hand.

The ultimate outcome of the conflict is uncertain. Iran has been a malign influence across the globe for 47 years, and any settlement that leaves it weakened but still able to control or meaningfully threaten the flow of shipping in and out of the Persian Gulf would be judged a major strategic failure. Such an outcome would call into question the principle of open navigation of the seas, a cornerstone of global commerce for decades. It would also represent a serious blow to US credibility and prestige, perhaps rivaling the reputational damage suffered by the British when Egypt seized the Suez Canal in 1956. We hope for a peaceful resolution, but the current ceasefire looks more like a pause than a conclusion, and we are not yet persuaded that the conflict has run its course.

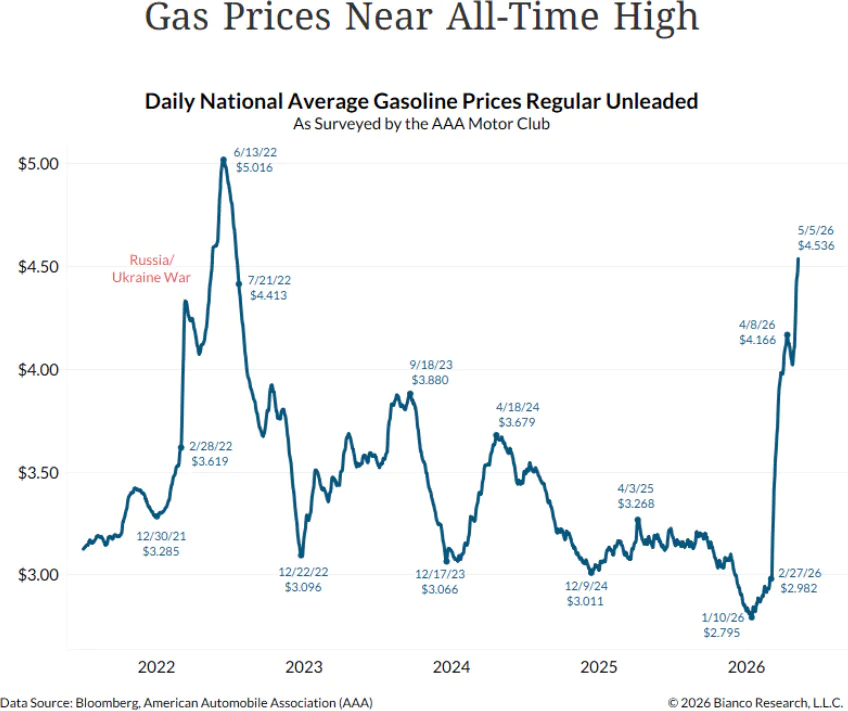

From an economic standpoint, global trade and energy markets have already been disrupted. Prior to the conflict, roughly 20% of the world’s oil passed through the Strait of Hormuz each day, underscoring just how strategically important this narrow shipping lane remains. While some workarounds exist, including pipelines that can transport oil to the Red Sea, those alternatives are limited and cannot fully replace normal maritime flows. Moreover, the disruption extends beyond crude oil. Other important commodity supply chains, including helium and fertilizer, have also been sharply curtailed, creating knock-on effects across industrial production, agriculture, and transportation. Prices have predictably spiked, inventories are being drawn down, and businesses are once again being reminded of how fragile global supply chains can be when geopolitical risks intensify.

The ceasefire announcement caused a sharp drop in prices, but markets for these key commodities remain far from normalized. Volatility remains elevated, and it would be premature to assume that a temporary easing in prices means the underlying risk has disappeared. The conceit of the Trump administration that these developments do not materially affect the US because we are energy independent ignores the global nature of energy and commodity markets. Oil may be produced domestically, but it is still priced in a global market, and disruptions abroad inevitably influence prices at home. Sharp increases in everything from gasoline to jet fuel domestically have already demonstrated that point. For most Americans, the most visible pain pump comes at the gas pump:

While we remain confident that the US economy has sufficient momentum to absorb the initial shock of higher energy prices, the duration of the conflict will likely be the ultimate determinant of the economic damage. A short disruption can often be weathered; a prolonged conflict is far more likely to erode business confidence, pressure household budgets, and complicate the path for inflation and interest rates. All wars end, and this one will not be an exception, so we are cautious about overreacting to emotional headlines that are often incomplete, inconsistent, or simply wrong. We remain attentive to new developments, focused on separating signal from noise, and prepared to make recommendations to you as circumstances evolve.

How Have Markets Reacted

The shock and awe of the military campaign may not have led to regime change in Iran, but it did upend the markets for a brief period. Stocks retreated sharply as investors grappled with the outlook. While this return made some sense, other asset reactions were counterintuitive. Those unexpected outcomes are of particular interest.

The initial equity market selloff was predictable. Sell first and ask questions later seemed to be the guiding principle for much of March. As the prospect of an end to hostilities increased, the equity markets began to stabilize. The announcement of the initial ceasefire led to a furious rally that has carried over into May and recovered all of the broad market declines.

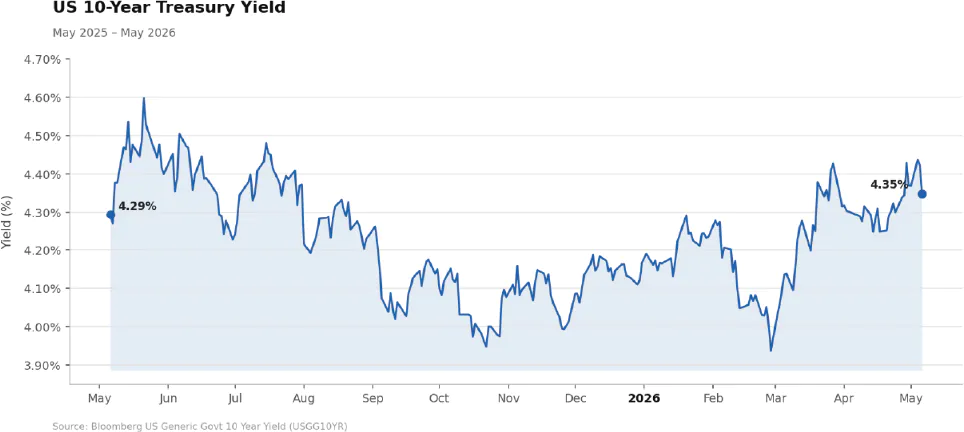

While equities have recovered, the bond market has not. In times of global instability, investors typically flock to fixed-income securities in the “flight to quality” trade. In the past month, however, the benchmark 10-year Treasury yield has risen from under 4% in late February to 4.3%. While the absolute move isn’t huge, the direction of travel is noteworthy. We believe that this increase in rates reflects investor fears about the inflationary impact of the conflict. The impact of higher oil prices may be transitory, but war is inflationary. Restocking munitions and armaments and rebuilding from the destruction of conflict don’t increase productivity. It simply pushes up costs, and the bond market seems to be sniffing out that risk.

Perhaps the biggest surprise was the sharp correction in gold prices. After a double-digit gain in February, gold retreated in March. Gold is often billed as a safe haven, not only from inflation but also from chaos in general. While that tends to be the case over longer horizons, in the short run, gold was a source of funds in March. Many investors, particularly in the Middle East, appeared to liquidate gold as the bombing began. As with equities, prices have stabilized (though not fully recovered).

We highlight these short-term moves not because they are actionable or helpful in making decisions. Instead, the range of outcomes over the short term reinforces the idea that diversification and time mitigate risk, not emotional reactions to volatile price action.

Other Investor Concerns

Before the Iran war began, investors were digesting important developments in other areas of the market. The first came in early February when Anthropic released its latest version of Claude, its AI model. Claude showed enormous progress in its ability to write software code with verbal prompts. The output is impressive and offers the potential for enormous advances in ease of use and potential cost savings for software users. One man’s savings, however, is another man’s business disrupted. Markets turned on software companies, long a darling of Wall Street because of their steady and recurring revenues. Seemingly overnight, the equity and debt securities of software companies were deemed toxic. While the threat to some software companies is very real, many other enterprise software offerings seem comparatively immune. The wave of change will come ashore, but its timing and magnitude are to be determined, and it seems that the baby may have been tossed out with the proverbial bathwater. Profound change creates risk and opportunity.

The market reaction in software may signal a shift in the AI investment thesis. Since the rollout of OpenAI in November 2022, the market has rewarded “picks and shovels” providers. The companies building data centers (e.g., Amazon and Microsoft), developing large language models (e.g., Meta and Google), and the chipmakers (e.g., Nvidia) were the preferred way to gain exposure to the theme. For the last six months, however, those stocks have stalled. The software story illustrates the transition to AI’s disruptive nature.

Who will win and who will lose? Perhaps the winners are the financial services companies like Rocket Mortgage that are becoming more efficient. Rocket reports that AI reduces the time required to process a mortgage application and supporting documents from four hours to fifteen minutes. A loser might be a software provider like Morningstar, the investment data provider whose shares have fallen nearly 50% in the past year, as the process of gathering, organizing, and analyzing data seems ripe for AI disruption. These examples aren’t recommendations; they highlight the opportunities and pitfalls that are likely to come into focus as AI adoption increases.

The second lightning bolt came from the US Supreme Court. In a long-anticipated decision, the Court ruled that President Trump exceeded his authority in imposing tariffs under the designation of economic emergency. We agree with the decision and reasoning. For the economy, markets, and global trade, the ruling adds more confusion. Will collected tariffs be refunded? When and how? Will the emergency tariffs be replaced? The answer to this question is yes, as the President cited a different statute to impose 10% tariffs on Friday of the decision, with a jump to a 15% tariff rate on Saturday. These tariffs have been challenged in court, so their future remains uncertain. Moreover, the duration of these tariffs is limited to just five months, even if the courts uphold their imposition. How does a business plan? What comes of separate agreements reached with trading partners? It all feels as clear as it did after Liberation Day, which is to say nothing is clear.

Where do we go for the rest of the year?

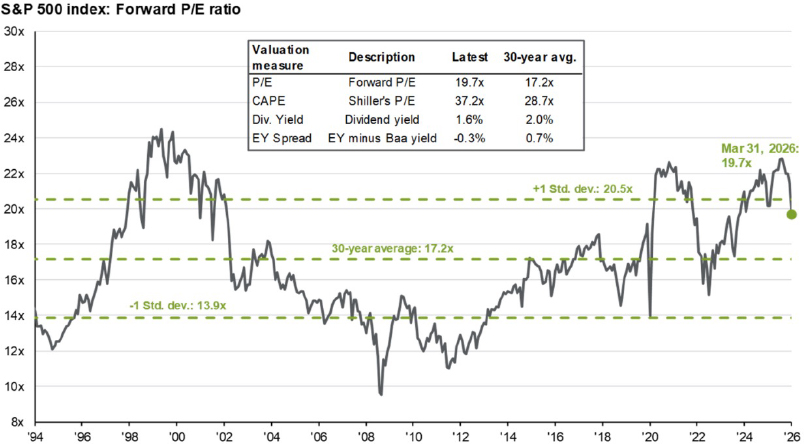

We aren’t in the prediction business. As Yogi Bera noted, it is tough to make predictions, especially about the future. In the short term, many factors drive asset prices. Over the medium to long term, however, fundamentals inevitably carry the day. The March pullback in prices has improved equity market valuations, as highlighted below in the chart from JPMorgan:

For equity investors, the good news is that PE multiples have actually remained steady into May because corporate earnings have been so strong. More importantly, earnings prospects are strong. While it may be that forecasts are too optimistic, higher earnings are likely to be supportive of equities in the second quarter:

Scary geopolitical headlines, political division, and chaos capture investor attention, but the breadth and magnitude of corporate profitability are the underappreciated story. Equally important, as shown in the graph, forecast earnings are also strong. Against that backdrop, it is hard to bet on a US recession. Given the uncertainties of the conflict and the wild reactions that markets have had to news flow, we will remain attentive to new developments but careful not to overreact.

Up Next...