A chaotic and uncertain world has become dramatically more uncertain in the last two weeks. A strong 2025 for investors carried over into 2026. However, February has seen three dramatic developments that are likely to define how the rest of the year plays out.

The first came in early February when Anthropic released its latest version of Claude, its AI model. Claude showed enormous progress in its ability to write software code with verbal prompts. The output is impressive and offers the potential for enormous advances in ease of use and potential cost savings for software users. One man’s savings, however, is another man’s business disrupted. Markets turned on software companies, long a darling of Wall Street because of their steady and recurring revenues. Seemingly overnight, the equity and debt securities of software companies were deemed toxic. While the threat to some software companies is very real, many other enterprise software offerings seem comparatively immune. The wave of change will come ashore, but its timing and magnitude are to be determined, and it seems that the baby may have been tossed out with the proverbial bathwater. Profound change creates risk and opportunity.

The second lightning bolt came from the US Supreme Court. In a long-anticipated decision, the Court ruled that President Trump exceeded his authority in imposing tariffs under the designation of economic emergency. We agree with the decision and reasoning. For the economy, markets, and global trade, the ruling adds more confusion. Will collected tariffs be refunded? When and how? Will the emergency tariffs be replaced? The answer to this question is yes, as the President cited a different statute to impose 10% tariffs on the Friday of the decision, with a jump to a 15% tariff rate on Saturday. These tariffs have been challenged in court, so their future remains uncertain. Moreover, the duration of these tariffs is limited to just five months, even if the courts uphold their imposition. How does a business plan? What comes of separate agreements reached with trading partners? It all feels as clear as it did after Liberation Day, which is to say nothing is clear.

The third and most profound development occurred in the Middle East as the United States and Israel attacked Iran with a dramatic “shock and awe” bombing campaign. The Iranian leadership was decapitated on the first day without a clear line of succession. Iran retaliated with missile and drone attacks throughout the Middle East, targeting many countries that were ostensibly neutral in the conflict. The duration and ultimate outcome are uncertain. Will there be regime change in Iran? Will the country be neutered and unable to project force and support terrorism?

From an economic standpoint, global trade and energy markets have been disrupted. The Strait of Hormuz, the key chokepoint for the export of Middle Eastern oil and gas, has seen a collapse of traffic, and energy production is being shut in as storage capacity in producing countries is quickly filled. While there are questions about the safety of passage, the more immediate issue is the inability to insure ships passing through the Strait at reasonable prices. Until this issue is resolved, energy markets will remain under short-term pressure.

As we write, Brent Crude has moved above $90 per barrel. Futures anticipate this disruption being short-lived, but until oil prices stabilize and then fall back to pre-conflict levels, financial markets will remain volatile. The good news is that the global economy was strengthening as the conflict began. All wars end, and this one seems likely to end soon because both sides are likely to run out of munitions. While geopolitics may be permanently altered, we don’t think the damage to the global economy will be permanent, so we are cautious about overreacting to emotional headlines that are often incomplete or wrong. We remain attuned to new developments and will make recommendations to you as circumstances dictate.

A Brief Look Back at 2025

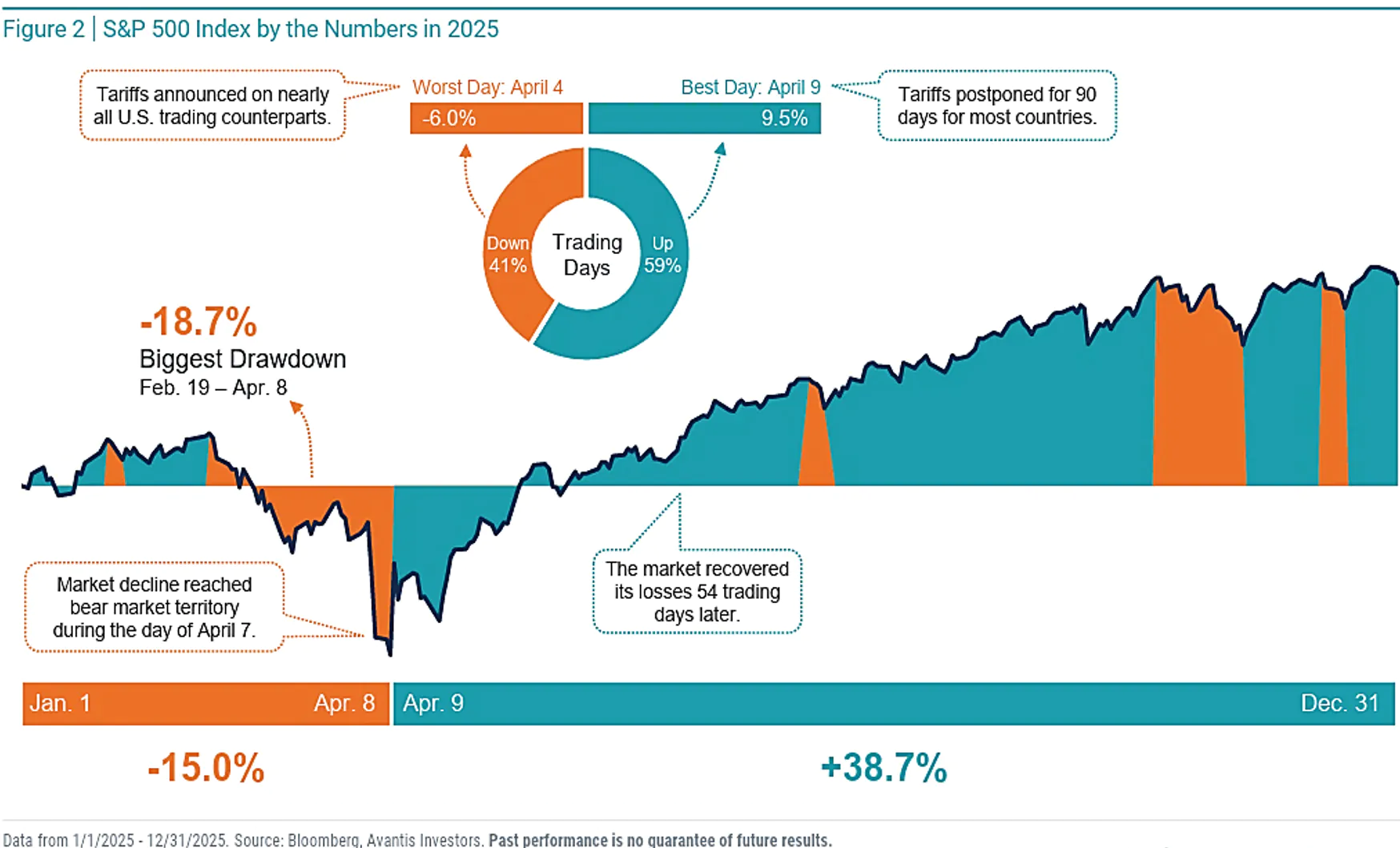

In looking back, despite the turmoil of 2025, it was a year that actually reinforced many time-tested principles. First, and most importantly, volatility is a part of investing. The 2025 rollercoaster illustrated below highlights the wild swings. April was particularly turbulent as tariff announcements, followed quickly by the administration’s backtracking, created huge up and down swings within the same week.

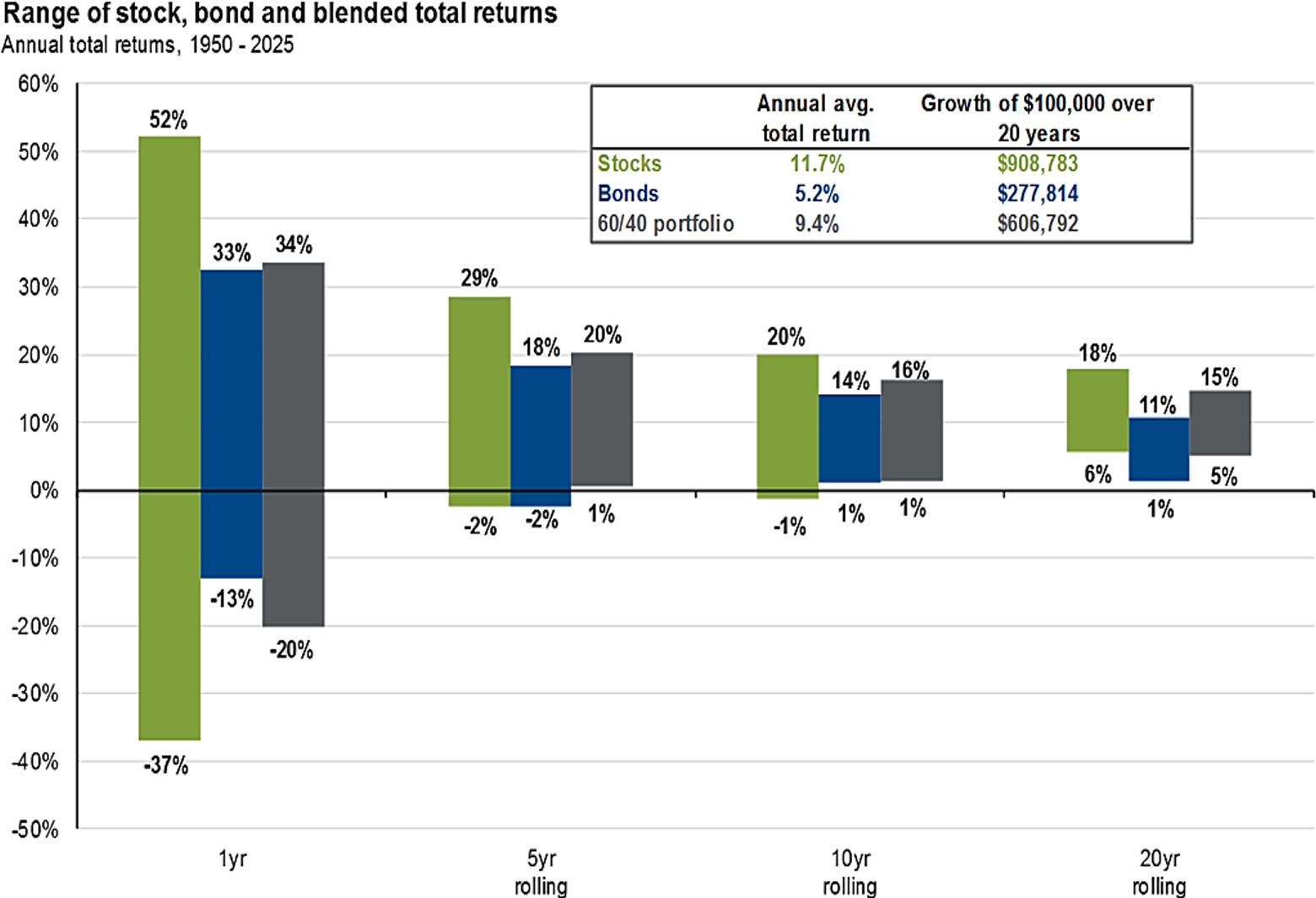

While these swings were very dramatic, they are not at all unusual. JP Morgan has a terrific chart to help maintain some perspective on annual market returns compared to the worst drawdowns during each calendar year:

This highlights the fact that volatility in equities is simply the price investors must pay for the growth potential of equities. Because this level of volatility can be so unnerving, investors who don’t want the wild ride have different choices. Some endeavor to time the market by jumping in and out. This has always and everywhere proven to be a fool’s errand.

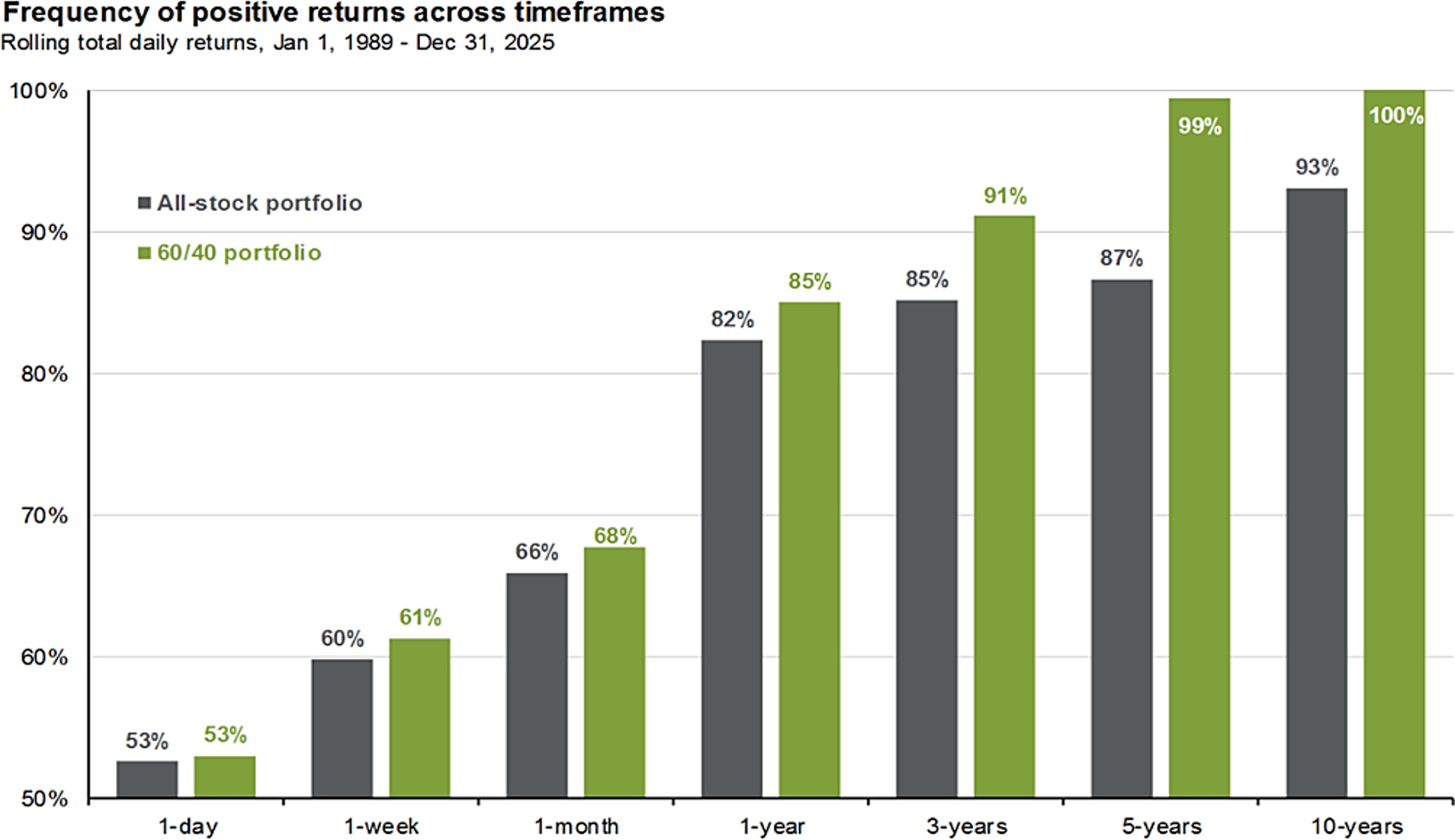

More successful investors rely on time (i.e., longer holding periods smooth returns) and diversification (combining assets with low correlations to improve returns:

An alternative way to consider the benefits of diversification and holding period is to analyze the frequency of positive returns. On a given day or week, the results for an all-stock portfolio versus a diversified portfolio are a coin toss. For every long-term period, however, diversification meaningfully reduces the likelihood of negative returns:

The 2026 Outlook

The advancing and broadening stock market of late 2025 has given way to the apprehension and uncertainty that conflict always produces. In considering what the balance of the year may hold, it is easy to get lost in the blizzard of data and conflicting views. We would draw your attention to four observations, beginning with valuation.

As we have discussed often, equity market valuations are rich. That simple and widely known fact tells us little about how markets may behave in the coming year because value is a terrible short-term indicator. Overvalued assets can remain overvalued and become more overvalued for longer than anyone can imagine. Similarly, undervalued assets can remain “cheap” for longer than an investor can bear. What valuations do hint at is the extent of risk embedded in markets.

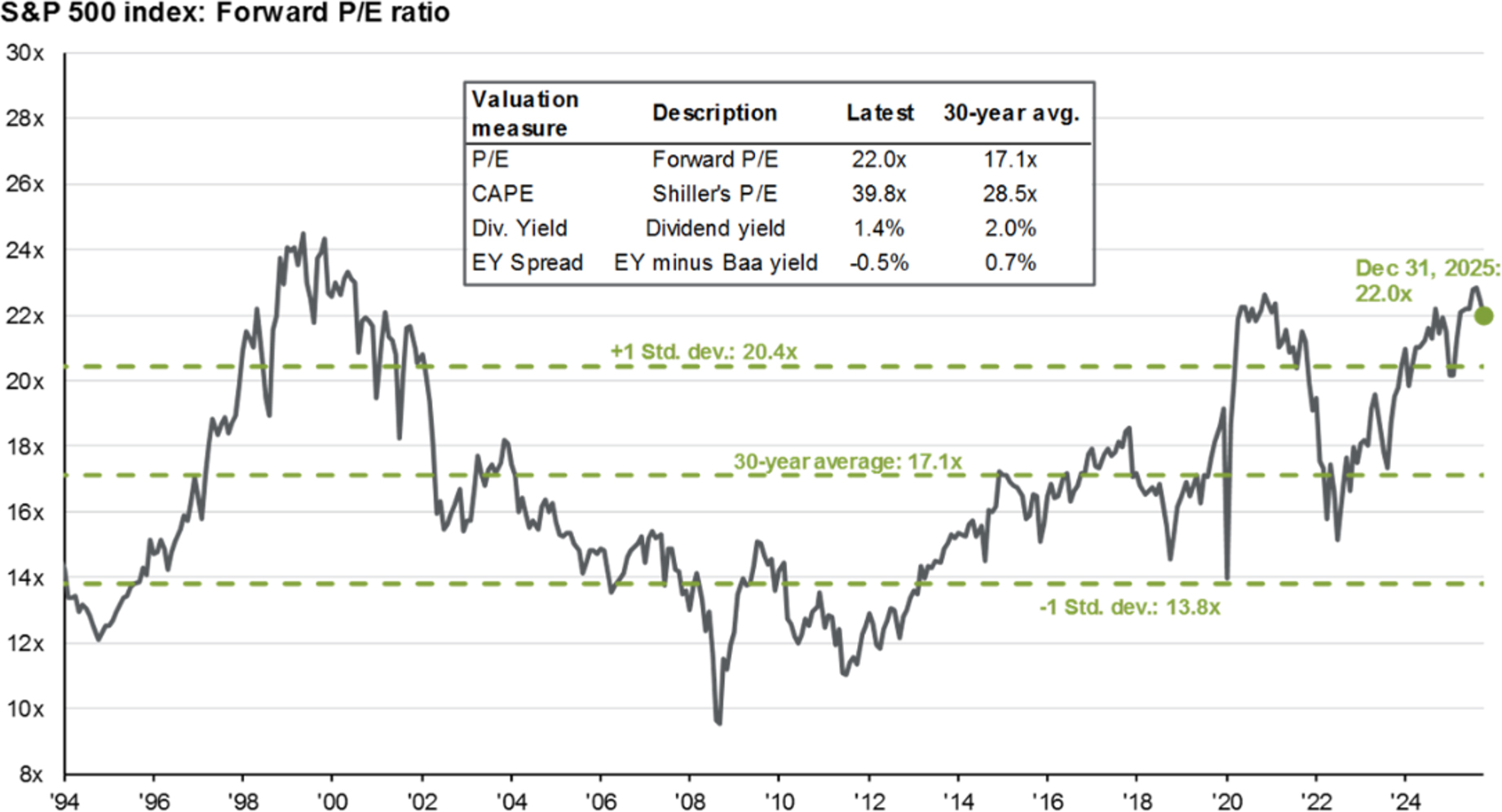

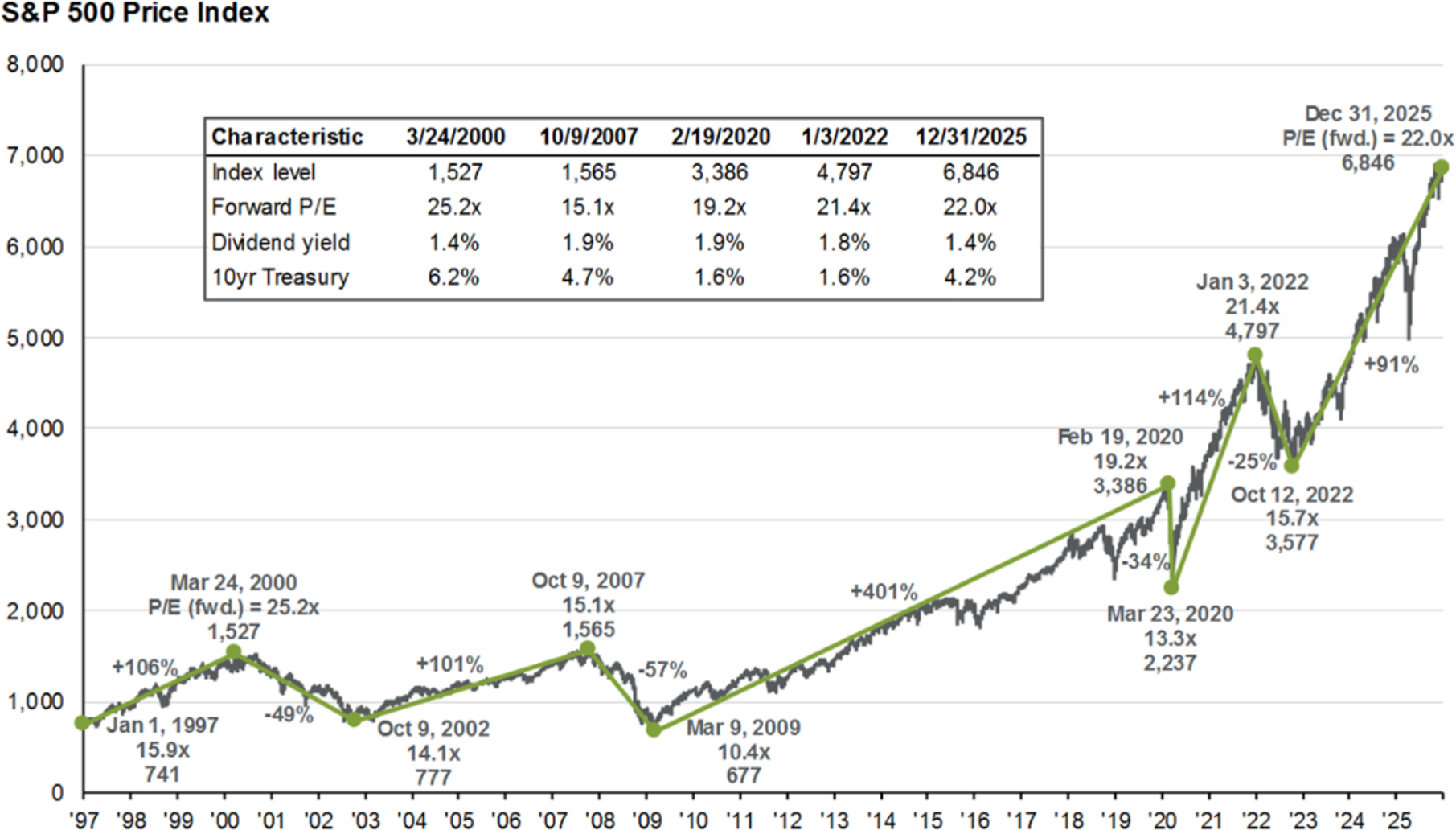

At year’s end, the S&P 500 traded at a forward price earnings (PE) ratio of 22:

It is interesting to look back and compare this and other valuation metrics at critical market junctures. At the beginning of the 2022 bear market, the forward PE was 21.4 times. This suggests that market gains over the past four years came primarily from strong earnings growth for US companies:

This observation, that earnings growth has remained strong despite elections, wars, tariffs, inflation, and interest rate changes, is what gives us optimism about 2026. The combination of modest inflation, strong expected earnings growth, and lower interest rates makes it hard to bet against equities in the coming year.

With respect to inflation, we have been nervous about it for some time, and we still fret about massive government deficits as a driver of higher prices. Inflation was trending lower at the start of the year, but the conflict in the Middle East has pushed up oil and pump prices. What looked like a strong tailwind has become a headwind of uncertain duration.

Earnings growth is forecast to be in the range of 15% this year. Early-year forecasts are notoriously optimistic, but double-digit earnings growth doesn’t seem like an unreasonable expectation, and that earnings growth is the ultimate driver of equity prices.

Finally, the Fed has cut interest rates three times since the fall, and markets anticipate two more rate cuts in 2026. With a new Federal Reserve chair likely to do the bidding of the administration, it seems likely that rates will be lower this year.

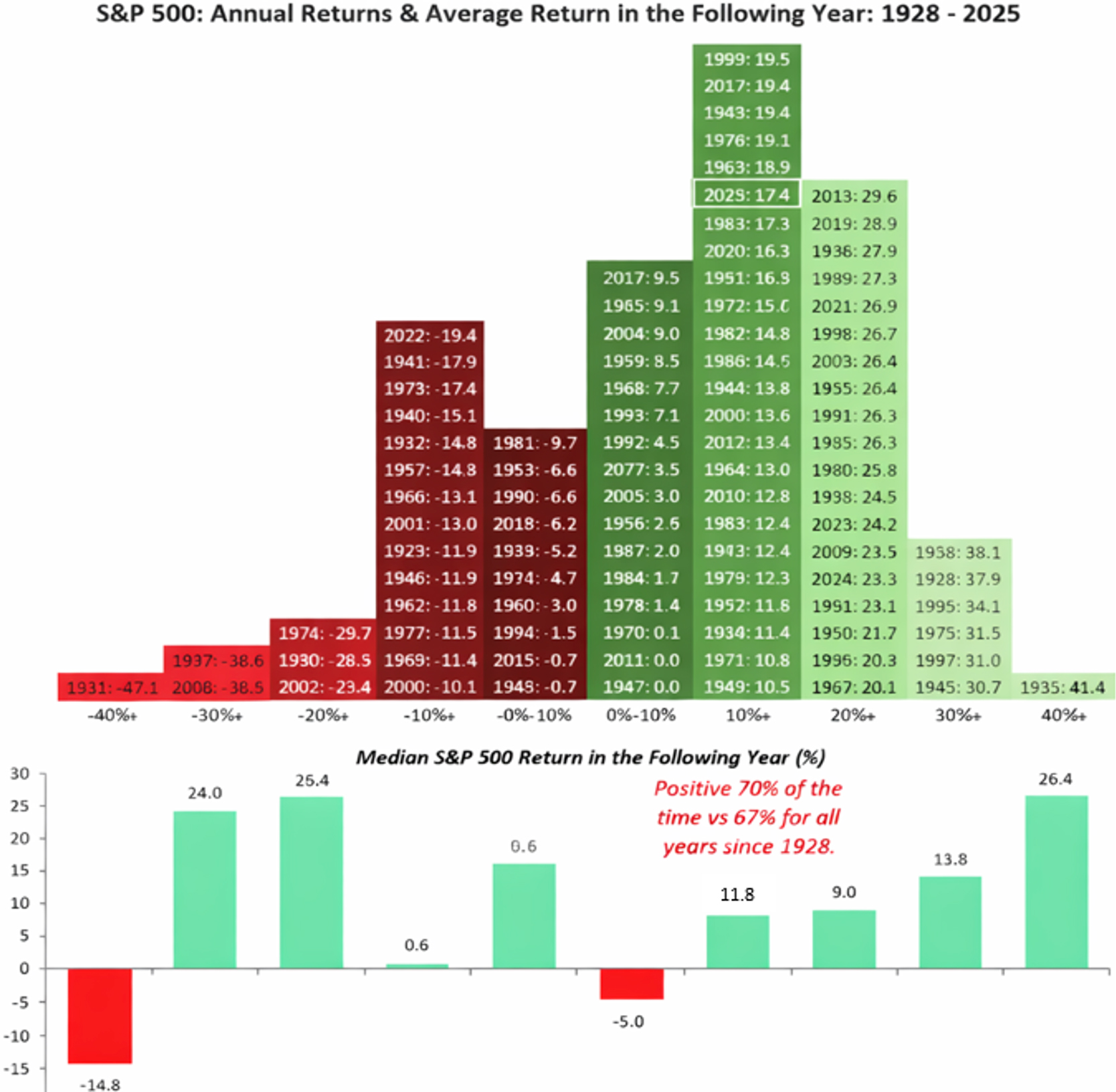

Taken together, lower inflation, higher earnings, and declining rates point to higher equity prices. The second year of a Presidential cycle typically isn’t the best for equities, but momentum is a powerful and potentially offsetting force. As Bespoke points out in the chart below, years of double-digit returns are followed by double-digit returns 70% of the time.

Our optimism is tempered by starting valuations, so our focus in the new year will be on further diversifying portfolios and keeping a close eye on liquidity needs. During tumultuous times, focus, discipline, and patience create the opportunity for success.

Summary

2025 was a memorable year in so many ways. It was an excellent year for investors and one that underscored the principles that we apply in managing your portfolio. As 2026 unfolds, we look forward to the continued opportunity to be of service and welcome your thoughts, questions, and concerns. We are also looking ahead to the 2025 tax filing season. As tax data begins to roll into your mailboxes, we would encourage you to be patient and allow for the receipt of all of your data, including corrected 1099s. Filing early often requires amendments later, so patience is a virtue in preparing for filing for 2025.

Up Next...